Every pitch deck ends the same way. A slide titled "Exit," a logo soup of plausible acquirers, and a line about a five-to-seven year horizon to a "liquidity event." It is the part of the story everyone nods along to and no one checks.

We checked. Dealum sits on the portfolio records of more than 180 angel networks with thousands of investments logged not by a research team writing a report, but by the people who actually wrote the cheques. It is a dataset that captures what happens after the round closes, including the part of the story that rarely makes it into a conference panel: the companies that raised once and then went no further.

The picture it paints is not the one on the slide.

But it is not all bad news. Most of these companies never found a buyer — yet many of them are solid, working businesses. The way out is to widen the exit: instead of waiting for an IPO or a big-corporate acquisition, these startups can sell to, or partner with established mid-market companies, buyers that need exactly what they have already built and that almost nobody is watching. We will get to that at the end. First, the numbers.

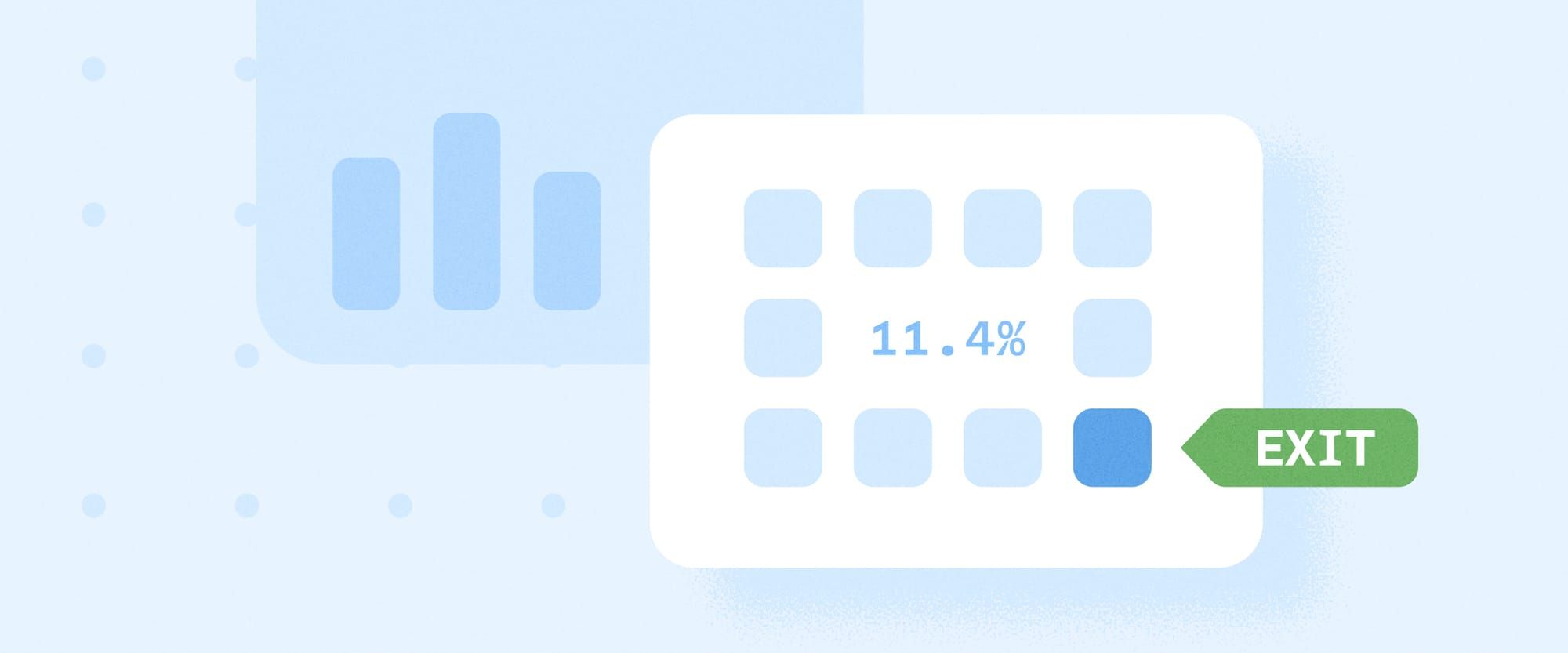

Just over one in ten

Across roughly 7,100 portfolio companies — the ones an investor on the platform has recorded an investment in — 11.4% have recorded an exit. Close to nine in ten have not.

That number deserves to sit on its own for a second, because it is the figure the industry is least comfortable saying out loud. Not nine in ten have failed — many are alive, growing, and perfectly healthy. But only 11.4% have produced the event the entire model is built around: the moment capital turns back into returns.

For the ones that do exit, the timeline is at least honest about itself. The average time from first investment to exit is 4.4 years. That is not far off the pitch-deck promise, for the companies that make it. The catch is the denominator. A 4.4-year average to exit is a comforting statistic right up until you remember it describes barely one company in ten.

What the data actually shows

The interesting part of the data isn't the companies that visibly shut down — those are rare in the records. What's far more common never announces itself at all: a company raises, and then nothing further appears on the record. No follow-on round, no sale, no liquidity event. Just silence.

The clearest signal is the funding funnel, and it collapses fast:

- 69.5% of companies raised once and never recorded another round.

- 30.5% made it to a second round.

- 14.8% reached a third.

- 8.5% reached a fourth.

Raising again isn't automatically the goal. Plenty of companies deliberately stop, having reached profitability or chosen not to dilute further. But it does show how few travel the full multi-round venture path the model is built around. For most companies, the seed round is the whole journey, not the start of one.

Among the companies where the timeline is visible, roughly 54% have shown no movement, no exit, no new funding for three years or more. For nearly a third, it has been more than five. We can't see how these companies are doing day to day. Many on this list may be performing perfectly well. But on the record, nothing has moved, and the original capital is still in place. That is the real shape of the gap: not a cliff, but a fade.

The capital that hasn't come back

Stack the timelines up, and the liquidity problem becomes physical.

For companies that haven't exited, the average holding period is already nearly six years and counting — well beyond the time it takes the successful 11% to reach an exit. Nearly half of all unexited companies have been held for over five years; close to a third for more than seven. The clock doesn't stop when a company goes quiet. It just keeps running on capital that isn't moving.

The consequence shows up on the balance sheet. Roughly 85% of all the capital recorded on our platform is tied up in companies that have not exited. That is not a portfolio of bets waiting to mature. For a large chunk of it, it is a portfolio of positions that have stopped maturing — not because the businesses behind them are worthless, but because the market that would buy them is missing — and that likely haven't been marked to reflect it.

The same story, market-wide

None of this is unique to our customers as it is the market they invest in. Venture-backed IPOs in the US, the headline route to liquidity, collapsed from 311 in 2021 to 38 in 2022 and have barely recovered since,[1] leaving capital stuck in private portfolios across the asset class. The National Venture Capital Association has gone as far as warning of an emerging cohort of "zombie companies" — businesses ticking along but with no credible exit in sight.[2] That is the same pattern our data shows, named by the industry's own trade body: a low exit rate isn't a verdict on any one network's picking, it's the structural condition of early-stage investing right now.

So what does this mean?

The uncomfortable conclusion is not that early-stage investing is risky. Everyone signs up for the risk. It is that the liquidity timeline everyone underwrites doesn't hold, in today's market, for the overwhelming majority of the portfolio.

Investors are holding illiquid positions for years longer than the model assumes, while the routes that would clear that backlog keep narrowing. The one in ten that exit do roughly what the deck promised. We've written before about how to plan for that exit. The rest are the part of the asset class no one prices honestly, because doing so would mean admitting how much capital is sitting still.

The data doesn't say early-stage investing is broken. It says the exit is the exception, not the plan and that the gap between the two is where the money is stuck.

The overlooked opportunity

But "stuck" assumes there's only one way out. Most of these companies were built for a venture-style exit. An IPO or a large strategic acquirer and that route has narrowed for everyone. That doesn't make them failures. It makes them a large, overlooked pool of solid businesses sitting just outside the one exit the industry keeps watching.

The question worth asking isn't why they haven't exited, it's who else might want what they've built. Large corporates already have an answer: startup scouting, venture clienting, and acquisition programs are standing functions of their innovation strategy. Mid-market companies face the same growth pressures, new capabilities, new technology, new markets, and no fast way to build them internally, but rarely have the corporate development teams to act on them.

That is the connection this data points to. On one side, thousands of businesses with proven teams and working technology, waiting on an exit route that has narrowed. On the other, mid-market companies that need exactly those things and can't build them fast enough. Neither side can easily see the other.

How that gap gets bridged and what it means for the companies on both sides of it is where the next post picks up.

Footnotes

- Jay R. Ritter, "Initial Public Offerings: VC-backed IPO Statistics Through 2025," University of Florida (Warrington College of Business), updated 2026 — https://site.warrington.ufl.edu/ritter/files/IPOs-VC-backed.pdf

- National Venture Capital Association 2024 Yearbook (produced with PitchBook), reported via CNBC, "IPO market gets boost from Circle's surge," 3 July 2025 — https://www.cnbc.com/2025/07/03/ipo-market-boost-from-circle-500percent-surge-vcs-say-drought-may-be-ending.html